The 10 Best Savings Accounts in Ireland

They say that money doesn’t grow on trees. It can, however, grow through smart investing, or by simply starting a savings account.

Opening a savings account is the easiest way to store or invest your hard-earned cash. Sure interest rates may not be as high, but they’re guaranteed to make your money grow risk-free.

Look no further, we’ve done all the research and rounded up the best savings accounts in Ireland here for you. We’ll also discuss some tips, along with answers to FAQs, to consider before opening an account.

Comparison of Interest Rates

One of the most important factors to consider before opening a savings account is its annual interest rate. Below you’ll see each account’s published rates from 2021 to 2022.

Take note that the interest you’ll receive from the bank is subject to a Deposit Interest Retention Tax, which is 33% of the interest earned.

| BANK/SAVINGS ACCOUNT | INTEREST RATES |

| Ulster Bank — Special Interest Deposit Account | 0.85% AER |

| Ulster Bank — Home Saver | 0.85% AER |

| Bank of Ireland — GoalSaver | 0.25% AER |

| Ulster Bank — urFirst Account | 0.95% AER |

| Ireland State Savings — Instalment Savings | 3.5% AER total return |

The Best Savings Accounts in Ireland

In no particular order, take a look at our selection of the best savings accounts in Ireland!

1. bunq

Best Flexible Mobile Banking

| INTEREST RATE | USD & GBP: 2.26% EUR: 2.26% |

| INITIAL DEPOSIT/MAX. BALANCE | Do not have minimum nor maximum balance requirement |

| MONTHLY DEPOSIT | No specific requirement |

| WEBSITE | https://www.bunq.com |

Easy Savings

bunq Free

bunq Core

bunq Pro

bunq Elite

Business

bunq’s savings account offers a simple and effective way for businesses to grow their money, supported by attractive interest rates. With a competitive rate of 2.26% for new users (matching the bonus rate for existing users), bunq provides a strong incentive for maximizing savings in the current market.

The app’s user-friendly interface allows users to open a savings account in just minutes, with no minimum deposit required. bunq offers tailored solutions through its Easy Savings, Easy Bank Pro, and Easy Bank Pro XL accounts, catering to a range of business needs.

One of the key advantages of bunq’s savings account is the frequency of interest payouts. Interest is credited every week, enabling users to benefit from compound interest, which can significantly boost their savings over time. This feature, combined with a competitive interest rate, makes Bunq an appealing choice for businesses seeking efficient growth of their funds.

However, starting from November 6th, 2024, there will be an update to bunq’s base interest rate for Personal Savings Accounts, decreasing from 2.16% to 2.01%. Importantly, the 2.26% rate for new users remains unchanged. Additionally, there are no changes to the interest rates for Business Accounts. This adjustment applies across all regions.

The integration of the savings account with bunq’s broader banking services is another notable benefit. Users can seamlessly transfer money between their savings and checking accounts, utilize advanced budgeting tools, and set up multiple savings accounts for different financial goals. The streamlined sign-up process, which takes about 5 minutes, allows businesses to get started quickly.

Despite its strengths, bunq’s digital-only nature may not suit all users. The entire service is app-based, which could be challenging for businesses that prefer traditional banking options. Additionally, the reliance on internet connectivity may limit access in areas with poor service.

In conclusion, bunq’s savings account offers a high-interest, efficient, and user-friendly solution for growing funds. The frequent interest payouts and comprehensive integration with other services enhance its appeal, although the digital-only approach may not work for everyone. For businesses comfortable with a fully online banking experience, bunq provides a compelling choice. https://www.financeads.net/tc.php?t=56726C5042118028T

Pros

- Competitive interest rate of 2.26%

- Weekly interest payouts for compound growth

- Easy integration with other bunq banking services

- Multiple savings accounts for different goals

Cons

- Digital-only banking might not suit everyone

2. Raisin.com

Comprehensive Savings Account

| INTEREST RATE | Depends on the bank |

| INITIAL DEPOSIT/MAX. BALANCE | Min. amount: demand deposit account from 1€, deposit account: differs. Maximum balance: differs per bank |

| MONTHLY DEPOSIT | No specific requirement |

| WEBSITE | https://www.raisin.com/ |

Raisin is a European savings platform that has rapidly grown to become a major player in the financial services industry. With a mission to provide “savings without barriers,” Raisin has attracted over a million customers worldwide, who have collectively invested more than €60 billion across all Raisin platforms.

Unlike others, they provide access to a wide variety of savings products, including Term and Demand Deposit accounts, from over 16 partner banks. This diversity allows customers to choose the best options that fit their financial goals, whether they seek higher interest rates or more flexible terms.

Raisin’s main draw is to give Irish savers access to competitive interest rates from banks across Europe. By comparing numerous types of savings accounts from multiple banks, customers can often find better rates than those available in Ireland.

We also love how their platform allows users to manage all their savings accounts through a single interface, making it simple to keep track of investments. Raisin Bank ensures a smooth savings process, which includes everything from opening an account to transferring funds.

Furthermore, Raisin’s partner banks are fully regulated within the European Union, customers’ deposits are protected under the European Deposit Insurance Scheme (EDIS) up to €100,000 per bank (or an equivalent in the local currency). If you want to save higher amounts, you can easily spread your money across different banks, as the guarantee applies per bank, per person. This ensures peace of mind, knowing that your savings are secure.

Pros

- Diverse Range of Savings Accounts

- Competitive Interest Rates

- Manage multiple banks through one central account

- Regulatory Security

Cons

- No onsite offices

3. Klarna

Prompt Customer Service

| INTEREST RATE | 12m, 2.90% (up from 2.71%) 18m, 2.92% (up from 2.61%) 24m, 2.96% (up from 2.85%) 36m, 3.01% (up from 2.90%) 48m, 3.05% (up from 3.00%) |

| INITIAL DEPOSIT/MAX. BALANCE | Contact for more information |

| MONTHLY DEPOSIT | No specific requirement |

| WEBSITE | https://www.klarna.com/ie/fixed-savings/ |

Klarna, best known for its innovative payment solutions, is expanding its footprint in personal finance with the Klarna Fixed Savings Account—a secure, high-interest option for those who prefer guaranteed returns. Available through the Klarna app, this product combines flexibility, simplicity, and strong consumer protection under the Swedish deposit guarantee scheme.

Klarna’s fixed savings account allows users to lock in their preferred rate and term, ranging from 3 months to 48 months. Interest is fixed for the full duration, meaning savers can enjoy predictable, steady growth on their deposits without the uncertainty of rate fluctuations.

There are no account management or withdrawal fees, and no minimum deposit requirement, making the product accessible to both new savers and seasoned investors. Once the selected term ends, savers receive their full deposit plus the interest earned—ideal for anyone seeking a low-risk, hands-off saving approach.

Opening an account is quick and fully digital. Users can set up their Klarna balance through the app, navigate to the ‘Savings’ section, and open a fixed account in minutes. The app interface also allows savers to view their savings progress and term details at a glance.

Security remains a core feature: all deposits up to 1.150.000 SEK (approximately €105,000) are protected by the Swedish National Debt Office’s deposit guarantee scheme, ensuring peace of mind throughout the saving period.

With over 40 million Klarna app users worldwide, this fixed savings option extends Klarna’s reputation for reliability into long-term money management. For those seeking stable growth, transparent terms, and strong protection, Klarna’s Fixed Savings Account offers a modern and trustworthy way to build savings with confidence.

Pros

- No Fees, No Minimum Deposits

- Flexibility with Up to Three Accounts

- Easy Setup and Management

- Instant Access to Funds

- Integration with Klarna Balance and App Ecosystem

Cons

- Fairly New

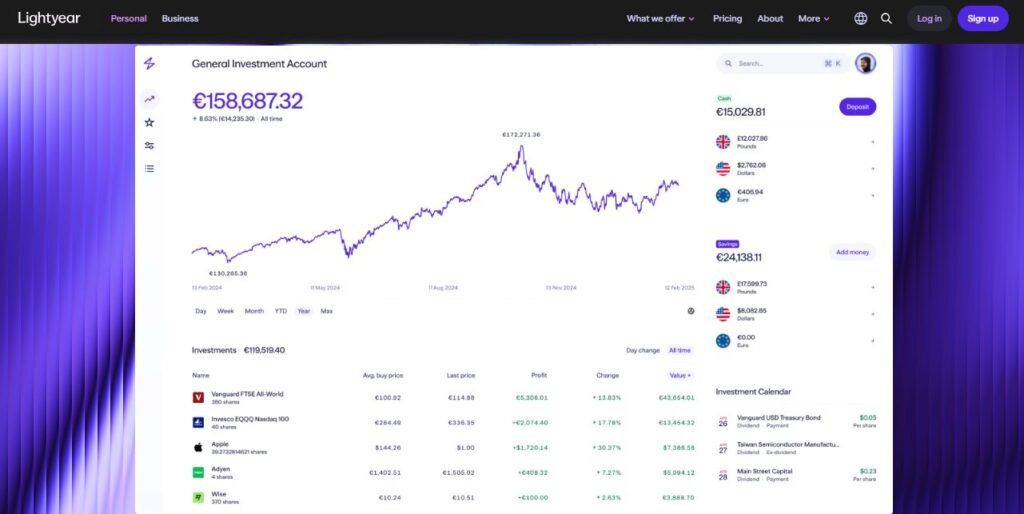

4. Lightyear

Best Savings Account Alternative

| INTEREST RATE | Up to 1% APY on EUR (rates vary by market conditions and customer location) Up to 3% APY on GBP (rates vary by market conditions and customer location) Up to 2.75% APY on USD for IE customers (effective since 18.12.2025, following the Fed rate decision |

| INITIAL DEPOSIT/MAX. BALANCE | Do not have minimum nor maximum balance requirement |

| MONTHLY DEPOSIT | Do not have monthly deposit requirement |

| WEBSITE | lightyear.com |

Lightyear stands out in the investment landscape with a user-centric platform designed to support smarter, more flexible investing. Its intuitive interface and thoughtful features make it appealing to both new and experienced investors.

One of Lightyear’s key strengths is access to live market data for the US and Germany, allowing users to make decisions based on real-time information. For other markets, prices are refreshed every 15 minutes, offering a practical balance between accuracy and efficiency.

Unlike many traditional investment platforms, Lightyear allows uninvested cash to earn interest rather than sitting idle. Interest rates vary by currency and market conditions, with competitive returns available on USD, GBP, and EUR balances.

For Irish customers, the interest rate on uninvested USD is currently 2.75% p.a. net, effective from 18 December 2025, following the US Federal Reserve’s latest rate decision. Rates are subject to change, and users are encouraged to check Lightyear’s website for the most up-to-date information.

Lightyear’s pricing model is transparent and easy to understand. Fees are kept low and clearly defined, including US shares at 0.1% per trade (capped at $1), EU shares at €1 per order, and UK shares at £1 per order, helping users manage costs without unexpected charges.

The platform also offers a multi-currency investment account, helping users reduce repeated foreign exchange conversions. Investors can hold multiple currencies, choose when to convert funds, and access a selection of ETFs with no execution fees (other fees may still apply), which can provide additional cost savings over time.

While Lightyear provides competitive interest rates on uninvested cash across major currencies, some higher rates—such as those available on certain regional currencies—may be limited to specific countries.

New users can sign up using the code BESTINIRELAND to receive up to €100 worth of a fractional share or ETF. Capital at risk, terms apply. Seek guidance if necessary.

Pros

- Licensed in Europe

- Interest on uninvested cash

- No hidden charges

- Real-time market data

- Diverse investment options

- User-Friendly Interface

- No double conversion fees

- Zero execution and custody fees for ETFs

- Over 6000 stocks and ETFs

- Have live data for DE and US and 15min for rest

Cons

- Limited research, technical analysis tools

5. Ulster Bank — Special Interest Deposit Account

Best Savings Account for Low-Income Earners

| INTEREST RATE | 0.85% AER (paid annually in October) |

| INITIAL DEPOSIT/MAX. BALANCE | €1 to €15,000 |

| MONTHLY DEPOSIT | €1,000 (max.) |

| WEBSITE | Ulster Bank SIDA |

If it’s your first time opening a savings account, Ulster Bank’s Special Interest Deposit Account (SIDA) is a great choice. You can open an account for as low as €1 from the comforts of your home or a branch nearest you.

Interest rates have hit rock bottom since the pandemic. Despite this, SIDA currently has one of the highest annual interest rates in the market at 0.85% AED.

While you may store up to €100,000 in your SIDA account, the maximum amount you may have in order to benefit from the interest rate is €15,000. Amounts higher than that would be subjected to lower interest rates.

Due to a standing order, this account may not be suitable for those who don’t have a steady monthly income. The good news is that you may only pay a minimum of €1 per month, which can be maxed out to €1,000.

Pros

- Low initial/monthly deposit amount

- Withdrawals permitted anytime

- Online banking available

- Relatively high-interest rates

Cons

- Has a minimum age requirement of 18 years old

- Low threshold for high-interest rates

6. Ulster Bank — Home Saver

Best Savings Account for First-time Home Buyers

| INTEREST RATE | 0.85% AER variable (paid annually in October) |

| INITIAL DEPOSIT/MAX. BALANCE | €1 to €25,000 |

| MONTHLY DEPOSIT | €2,500 (max.) |

| WEBSITE | Ulster Bank Home Saver |

Now, if you’re saving for a new home, you might want to check out Ulster Bank’s Home Saver account. Like our previous entry, it also boasts of a relatively high-interest rate of 0.85% AER.

First time home buyers may be eligible for a bonus interest of €2,000—a unique feature of this account. But before you get too excited, you might also want to check out their criteria on their website to see if you qualify.

The standing order also requires account holders to deposit anything from €1 to €2,500 monthly, which provides a bit of allowance for higher-income earners who wish to save more.

Comparing this to Ulster Bank’s SIDA, you have a slightly higher threshold of €25,000 in order to qualify for the higher interest rate. Any amount higher but not more than €100,000 is subject to a lower interest rate of 0.15% AED.

Pros

- Low initial/monthly deposit amount

- Withdrawals permitted anytime

- Online banking available

- Bonus interest may be gained

Cons

- Closed to regular account holders

- Has a minimum age requirement of 18 years old

7. Bank of Ireland — GoalSaver

Best Savings Account for Personal Current Account Holders

| INTEREST RATE | 0.25% AER variable (paid annually in March) |

| INITIAL DEPOSIT/MAX. BALANCE | €1 to €14,999 |

| MONTHLY DEPOSIT | €20 (min.) to €2,000 (max.) |

| WEBSITE | Bank of Ireland GoalSaver |

Next on our list is the Bank of Ireland’s GoalSaver account—a versatile savings account you can use to save for a new car, a holiday, or simply for a rainy day.

This year’s interest rates may have decreased to 0.25% AER due to the pandemic, but it remains to be one of the most decent rates in the market today.

Take note that you must already have an existing personal current account in the Republic of Ireland to open a GoalSaver account. If not, you may choose to open one with the Bank of Ireland, which only takes a few minutes to complete online or in your nearest branch.

Through direct debits, holders need to have sufficient balance in their personal current account to cover monthly payments for their GoalSaver account. So be sure to keep track of your accounts to avoid problems.

Pros

- Low initial/monthly deposit amount

- Withdrawals permitted anytime

- Online banking available

Cons

- Has a minimum age requirement of 18 years old

- Low threshold for high-interest rates

8. Ulster Bank — urFirst Account

Best Savings Account for Kids 11 And Under

| INTEREST RATE | 0.95% AER variable (paid quarterly) |

| INITIAL DEPOSIT/MAX. BALANCE | €5 (no maximum balance) |

| MONTHLY DEPOSIT | NA |

| WEBSITE | UR First Account |

For parents with kids under 11 years old, Ulster Bank’s urFirst Account is worth checking out. They currently have one of the highest interest rates for junior savings accounts in the market at 0.95% AER earned quarterly.

Your kids can already open an account with as little as €5 as the minimum balance. Furthermore, there are no limits on how much your kids can put in their accounts in order to qualify for the interest rate noted above.

What we like about urFirst Account is that kids are entitled to a free Henri Hippo moneybox, along with free learning materials available online, to encourage them to start saving early.

Keep in mind that kids above 12 years old won’t be entitled to this account. Instead, the bank may change their accounts to a urMoney, which you can learn more about on their website.

Pros

- Low maintaining balance

- Quarterly frequency of interest rates

- Free moneybox and educational materials

- Flexible deposit amounts allowed

Cons

- No ATM card

- Not suitable for 12 years old and above

9. Ireland State Savings — Instalment Savings

Best Savings Account for Long-Term Savers

| INTEREST RATE | 0.63% AER; total return of 3.5% upon maturity |

| MONTHLY DEPOSIT | €25 (min.) to €1,000 (max.) |

| WEBSITE | Ireland State Savings Instalment Savings |

If you’re thinking long term, you may also consider placing your money into Instalment Savings. Unlike other entries on our list, this account is a state savings product, meaning that you’re directly putting your hard-earned cash with the Irish Government.

In other words, the repayment of the principal amount and interest is an unconditional obligation of the Irish Government, so you can be sure that your money is secure and free from risk.

And because it is managed and protected by the State, Irish residents can also enjoy and receive a tax-free return. Holders of this product may pay a fixed minimum monthly instalment of €25 up to €1,000.

Perhaps the biggest catch is that there is a fixed 6-year term before you can receive its total return of 3.5%. You also have to inform them 7 days in advance should you decide to withdraw some cash, which may not be ideal for emergency situations.

While you can withdraw your cash early, bear in mind that your return will be lower than the published rates. Individuals aged below 18 years old may also be eligible for this product as long as their parent or guardian will provide written consent.

Pros

- High-interest rates

- Tax-free return

- No fees upon opening an account

- Low monthly deposit amount

Cons

- Has a fixed 6-year term

- 7-day notice period for withdrawals

- Online application unavailable for new applicants

FAQs about Savings Accounts in Ireland

And that’s it! We hope our guide simplified your process in finding the best savings account for you and your family in Ireland.

Think there’s another savings account worth mentioning too? Leave us a message and we’ll get back to you ASAP!

Likewise, we’ve also got you covered with our list of the best mortgage brokers in Dublin if you’re looking to buy your first home.